Seasons Greetings

Have a Nice Holiday!!!

posted by SmartYInvestor at 4:50 PM

0 comments

![]()

| · | My Blog | · | Oil | · | UOB KH | · | Photo | · | Data | · | SGX | · | S O Remisier | · | CNA | · | POEMS |

posted by SmartYInvestor at 12:08 PM

0 comments

![]()

posted by SmartYInvestor at 9:44 AM

0 comments

![]()

posted by SmartYInvestor at 9:19 PM

0 comments

![]()

posted by SmartYInvestor at 3:14 AM

0 comments

![]()

posted by SmartYInvestor at 10:12 PM

0 comments

![]()

posted by SmartYInvestor at 10:08 PM

0 comments

![]()

posted by SmartYInvestor at 10:04 PM

0 comments

![]()

posted by SmartYInvestor at 9:40 PM

0 comments

![]()

posted by SmartYInvestor at 5:21 PM

0 comments

![]()

posted by SmartYInvestor at 5:10 PM

0 comments

![]()

posted by SmartYInvestor at 4:54 PM

0 comments

![]()

posted by SmartYInvestor at 4:09 PM

0 comments

![]()

posted by SmartYInvestor at 2:14 PM

0 comments

![]()

posted by SmartYInvestor at 11:05 AM

0 comments

![]()

posted by SmartYInvestor at 7:30 AM

0 comments

![]()

posted by SmartYInvestor at 9:41 PM

0 comments

![]()

posted by SmartYInvestor at 6:12 PM

0 comments

![]()

posted by SmartYInvestor at 5:19 PM

0 comments

![]()

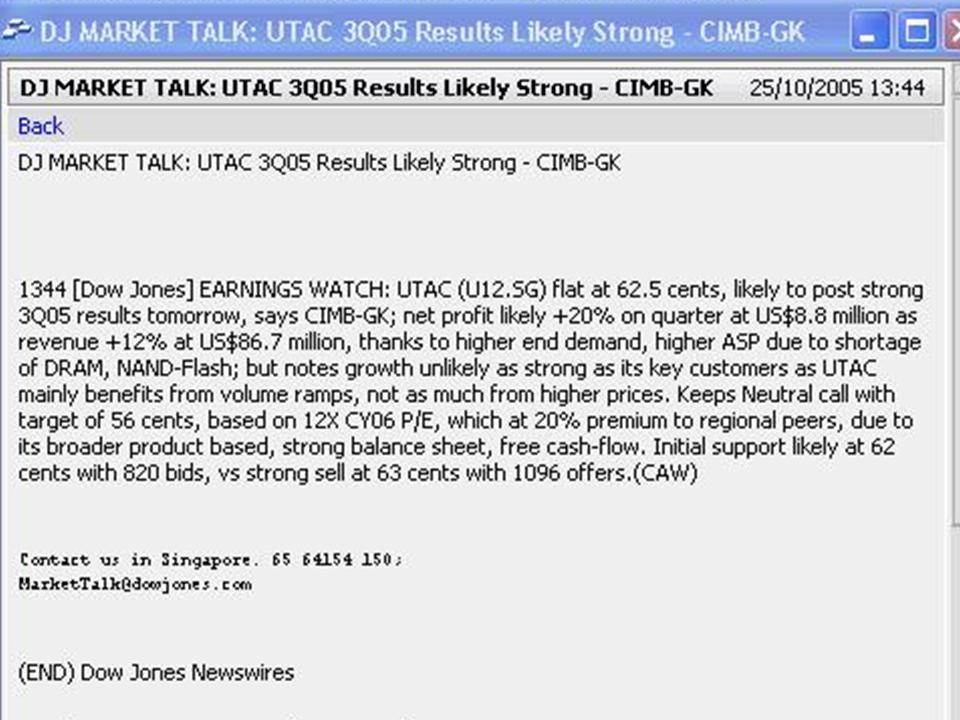

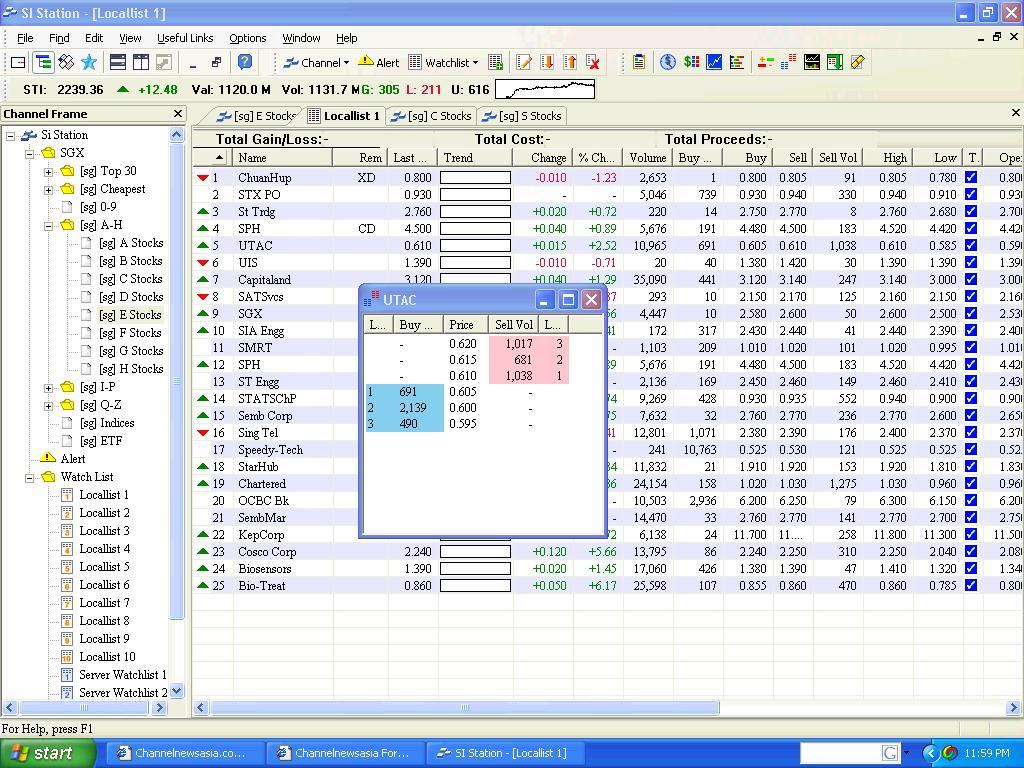

I already warned the weird pattern of UTAC in the past. So don't rush your luck too hard - it's a for "Long Position" only - a long haul game, punter!!

I already warned the weird pattern of UTAC in the past. So don't rush your luck too hard - it's a for "Long Position" only - a long haul game, punter!!

posted by SmartYInvestor at 2:25 PM

0 comments

![]()

Good news on UTAC will definitely boost price today. The question is: "Is it right to go in today and at what timing." Many amateurs would be emotionally geared to enter quickly without a proper plan strategy; I refer, particularly to inexperience punter or daytrader. The above is my would be plan!!

Good news on UTAC will definitely boost price today. The question is: "Is it right to go in today and at what timing." Many amateurs would be emotionally geared to enter quickly without a proper plan strategy; I refer, particularly to inexperience punter or daytrader. The above is my would be plan!!

posted by SmartYInvestor at 10:18 AM

0 comments

![]()

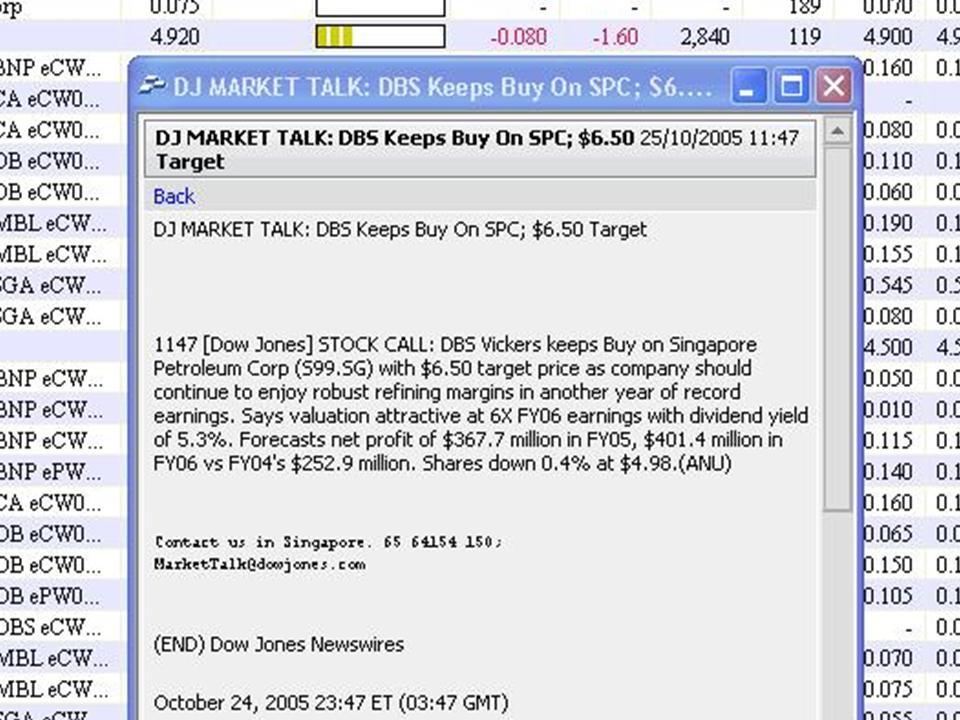

and remember all the tools available at all times! Buy only with the odds in your favour! Sound simple, you can bet, it is difficult to implement!!!

posted by SmartYInvestor at 8:24 PM

0 comments

![]()

posted by SmartYInvestor at 12:13 PM

0 comments

![]()

posted by SmartYInvestor at 9:02 AM

0 comments

![]()

posted by SmartYInvestor at 6:14 PM

0 comments

![]()

posted by SmartYInvestor at 5:05 PM

0 comments

![]()

posted by SmartYInvestor at 2:11 PM

0 comments

![]()

posted by SmartYInvestor at 1:20 PM

0 comments

![]()

posted by SmartYInvestor at 11:47 AM

0 comments

![]()

posted by SmartYInvestor at 11:35 AM

0 comments

![]()

posted by SmartYInvestor at 9:44 AM

0 comments

![]()

posted by SmartYInvestor at 8:53 AM

0 comments

![]()

posted by SmartYInvestor at 12:38 AM

0 comments

![]()

posted by SmartYInvestor at 11:54 PM

0 comments

![]()

posted by SmartYInvestor at 9:00 AM

0 comments

![]()

posted by SmartYInvestor at 3:28 PM

0 comments

![]()

posted by SmartYInvestor at 1:59 AM

0 comments

![]()

posted by SmartYInvestor at 1:08 AM

0 comments

![]()

posted by SmartYInvestor at 8:53 PM

0 comments

![]()

posted by SmartYInvestor at 3:36 PM

0 comments

![]()

posted by SmartYInvestor at 9:29 AM

0 comments

![]()

posted by SmartYInvestor at 11:51 PM

0 comments

![]()

posted by SmartYInvestor at 11:41 PM

0 comments

![]()

posted by SmartYInvestor at 11:35 PM

0 comments

![]()

posted by SmartYInvestor at 9:23 PM

0 comments

![]()

posted by SmartYInvestor at 7:08 PM

0 comments

![]()

posted by SmartYInvestor at 5:31 PM

0 comments

![]()

posted by SmartYInvestor at 5:55 PM

0 comments

![]()

posted by SmartYInvestor at 8:32 AM

0 comments

![]()

posted by SmartYInvestor at 9:44 PM

0 comments

![]()

posted by SmartYInvestor at 8:43 PM

0 comments

![]()

posted by SmartYInvestor at 12:02 PM

0 comments

![]()

posted by SmartYInvestor at 11:15 PM

0 comments

![]()

posted by SmartYInvestor at 8:43 PM

0 comments

![]()

Disclaimer: No document/material here is a solicitation to buy or sell. You are advised to think carefully and take your own responsibility for all consequences

|

|

|

|

|

|

|

|

|

|

|

|

|

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}